By M. Ray Perryman, PhD, CEO and President

Overview

The US economy continues to improve, with the pace of recovery linked to the pattern in COVID-19 cases. The virus and measures to slow its spread caused the disappearance of well over 22 million US jobs in just two months back in March and April of 2020. Each of these lost positions represented an associated reduction in income and financial security. For many families, the consequences included increased stress, hunger, and myriad other issues.

Employment/COVID Correlation

Hiring began to resume as the economy gradually reopened through the summer of 2020, and millions of jobs were restored (2.8 million in May, 4.8 million in June, 1.7 million in July, and 1.6 million in August). During that time, COVID-19 cases were generally trending in the 20-50,000 daily range. Much of the economy remained closed or curtailed, but enough had been learned to permit some progress.

During the fall of 2020, however, cases rose. It was a natural outgrowth of the restoration of activity and the properties of the virus, but uncertainty increased. Worse, hospitalizations and deaths rose sharply. Not surprisingly, the pace of job gains stalled, even turning negative in December 2020 (-306,000).

Cases dropped in early 2021, with vaccination programs rolling out and the virus better understood. Daily case levels fell from the 100,000 range in early February to about 55,000 in March, but rose to nearly 70,000 in April. Correspondingly, monthly job gains were 536,000 in February and 785,000 in March, falling to 269,000 in April. Summer 2021 saw national case numbers at their lowest point since the pandemic began; on June 19, 2021, the seven-day average reached 11,518. Job gains through the summer were again strong (962,000 in June and 1.1 million in July).

Cases ratcheted up through late summer 2021 with the Delta wave, topping 160,000 per day by September. The pace of job growth also fell, with 483,000 in August and 379,000 in September. As this variant waned, job growth again increased, up 648,000 in October. With the current Omicron surge, case numbers are the highest ever, and the economy is once again expanding at a notably slower rate. The bottom line is that as the virus increases, job growth slows. Until the health crisis is dealt with, uneven growth will be inevitable.

Conclusion

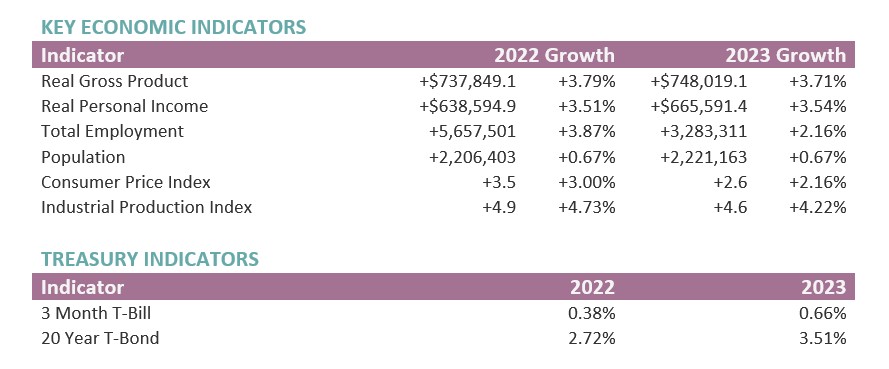

As we enter 2022, another challenge that continues is high inflation. While currently at levels not seen in decades, there are signs that upward pressure could be decreasing. With action by the Federal Reserve and easing of supply chain issues, the rate of price increases should slow. Despite these challenges, the US economy is expected to continue to recover and see significant growth. The Perryman Group’s most recent projections indicate real gross product is forecast to expand by +3.79% this year on a year-over-year basis, with +3.71% growth in 2023. Job gains are projected to be +5.658 million through 2022, with a gain of +3.283 million jobs next year.

About Dr. M. Ray Perryman and the Perryman Group

About Dr. M. Ray Perryman and the Perryman Group

Dr. M. Ray Perryman is President and Chief Executive Officer of The Perryman Group (www.perrymangroup.com). He also serves as Institute Distinguished Professor of Economic Theory and Method at the International Institute for Advanced Studies.