Investment Commentary – In our first quarter 2020 letter back in April, which feels like an eternity ago, we recognized that we were living through an incredible period of history. The pandemic weighed heavily on us then, as it does today. But this quarter, we look back at what we’ve endured and lay out our investment outlook for 2021 and beyond. While many risks remain, the effective vaccines that are starting to be distributed provide a real light at the end of the tunnel. We said in the first quarter that we would get through this crisis and that things would improve and recover. Financial markets recovered first, experiencing both their quickest decline and rebound on record, despite the significant global economic contraction. Economies have made great progress too but are not back to their pre-COVID-19 levels yet and may not be for another year or two. On the health side, despite the approval of several effective vaccines, it may take sometime before they can be widely distributed to the general populace. This may set back economies in the near term, but we expect that 2021 will see the end of the pandemic and our society can then follow markets and the economy in bouncing back as well.

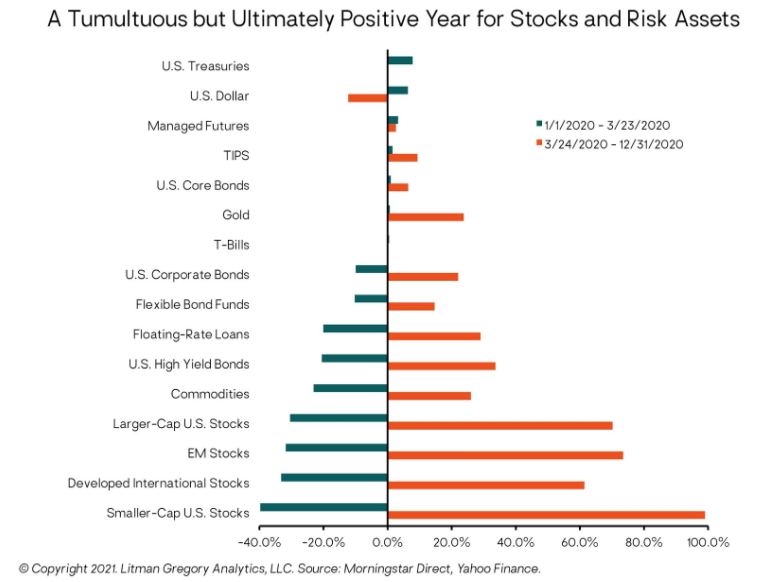

Looking Back – This year was a tragic one. Yet U.S. stocks did very well ending up 18.2%, while developed international stocks gained almost 10%. The comforting full-year returns mask the incredible volatility and stress investors faced earlier in the year. Stock markets around the world were down 30%–40% for the year by March 23, the year’s low point. From there, stocks skyrocketed into year-end. During the worst days of March, with pandemic fears rampant and the global economy falling off a cliff, very few predicted this year’s outsized performance for stocks. But our decision in mid-March to add an increment back to U.S. stocks added value, as the stock market is up roughly 50% since then. But while we did not foresee the market would rebound so far so quickly, we were confident that equity valuations had become more attractive, that expected returns had increased, and that it usually pays to be greedy when others are fearful. Another successful tactical allocation decision was our overweight position in emerging-market stocks, where valuations were more attractive and we had a higher conviction. Since May, emerging-market stocks have outperformed both European and U.S. stocks by roughly 10%.

Looking Ahead – The vaccines, easy financial conditions, and stimulative fiscal policy are all reasons for our optimism for society, the economy, and markets looking ahead. The likelihood of widespread vaccine distribution supports the case for a cyclical economic recovery beginning in the second and third quarter of 2021. Central bank monetary policy is almost certain to remain very accommodative for at least the next year or two and fiscal policy should be stimulative. This macro backdrop should be supportive of equities and other financial risk assets. U.S. stocks have high absolute valuations, but they do not look expensive relative to extremely low bond yields. In our view, non-U.S. stock markets, emerging-market stocks in particular, are more attractively valued and have higher expected returns than U.S. stocks over the next several years. We are slightly underweight to U.S. stocks and overweight to emerging-market stocks for this reason. It’s important to repeat that the plausible argument that low interest rates justify higher U.S. stock valuations is only more applicable overseas where stocks are even cheaper compared to bonds, which sport negative yields in some places. Currency is another potential tailwind for non-U.S. stocks over U.S. stocks. If the global economic recovery and an accommodative monetary policy plays out, we’d expect the U.S. dollar to continue its recent decline. As a “counter-cyclical” currency, the U.S. dollar tends to move in the opposite direction of global growth and investors in non-U.S. stocks will earn a currency return on top of any equity return.

Current Risks – As always, there are numerous risks to our economic/market base case. Unexpected shocks can happen at any time, whether a jump in inflation, domestic political dysfunction, geopolitical conflict, or trade disputes. Financial market history teaches us to expect the unexpected and expect to be surprised. Over the next few months, there is a real risk of a sharp economic slowdown from pandemic-induced lockdowns and, potentially, inadequate additional fiscal relief for households, small businesses, and state and local government budgets. The current extreme investor optimism also leaves the market vulnerable to disappointment. But given the positive macro and investment backdrop, we would likely view any financial market drawdowns as temporary.

Looking out longer term, the big risks we are watching are the specter of inflation and China. Inflation is a lower concern at this point, but the risk isn’t zero. Rising demand stemming from spending unleashed after the pandemic could coincide with a supply side constrained by the retreat of globalization to instigate an inflationary spiral. Clients should know that we have several asset classes and strategies in our portfolios—flexible bond strategies, floating-rate loans, alternative asset classes, and global stocks—that should do well in an inflationary environment. We also have other inflation-sensitive investment options at our disposal should we see the need for additional tactical protection. Turning to China, we are focused on the risk and opportunity it presents because of its outsized influence within the emerging markets. China has handled the pandemic relatively well and its stock market and economy have been some of the best performers in 2020. We wouldn’t be surprised to see stocks there pullback, especially as China reins in excesses and reduces stimulus. We also expect trade and tech conflicts to continue. But longer term, we remain bullish on China and emerging-market stocks in general. We think we are in the early stages of investors rebalancing their portfolios to increase non-U.S. equity exposure in order to partake of the benefits of global diversification.

Closing Thoughts – Our portfolios are well positioned for a cyclical recovery from the global pandemic, but our positioning always incorporates a wide range of potentialities. Should a less sanguine outcome occur, we have investments in the portfolio that can offer downside protection. And we are prepared to prudently, but opportunistically, respond as events unfold as we did in 2020. The market has always exhibited dramatic mood swings, whipsawing investor sentiment, and 2020 was no different. We recommend investors ignore the crowd’s actions and, as we closed our first quarter letter, “stay the course.” Better yet, be prepared to take advantage of the market’s mood swings, as we did this past year to our clients’ benefit. Our disciplined approach allowed us to do this successfully in 2020 on your behalf. We thank you for your continued trust in us and we wish everyone a healthy and blessed New Year! Please find the enclosed additional economic newsletter from Dr. Ray Perryman.

The Water Valley Investment Team