Market Recap

Never a dull news cycle! Investors were barraged with a staggering number of events during the quarter. There was no shortage of geopolitical headlines with the year kicking off with the capture and extradition of Venezuela’s then-president, Nicolás Maduro. And as the first quarter ends, conflict in the Middle East dominates the narrative and is roiling markets.

In the first quarter, domestic stocks fell 4.3%. U.S. equities were marginally positive on the year until the conflict with Iran commenced in late February. Since the onset of the war at the end of February, foreign equity markets have suffered worse than domestic markets. A stronger U.S. dollar in March contributed to some of the underperformance—another possible explanation is that higher energy prices have more of a negative impact on countries that import much of their energy. The U.S. has become a net exporter of oil in recent years and much less reliant on the Middle East for energy. Other nations, particularly many in Asia, import much of their energy through the Persian Gulf. Unsurprisingly, energy stocks (up 38.2%) were the top performer during the first quarter. More defensive sectors, such as utilities, also outperformed. Mega-cap tech stocks were the laggards during the first two months of 2026 as fears around elevated AI spend and a growing concern that many software stocks could see their moats weakened by AI agents. The S&P North American Expanded Technology Software Index has already fallen more than 24% this year and is now down in-excess of 30% from its high last September.

After delivering another rate cut last December, the Fed held rates steady at their two meetings in 2026. The Fed funds rate remains at 3.5%-3.75%. Since the onset of the conflict, the market has priced out any additional rate cuts this year. The implied number of cuts for 2026 was about two cuts at the end of February—however, the market is now pricing a Fed that will hold rates at current levels. Longer-dated bond rates have moved higher on fears of higher inflation stemming from the spike in energy prices. After closing below 4% at the end of February, the 10-year Treasury rate has jumped to nearly 4.4%. The two-year Treasury, which is often cited as a good proxy for the Fed funds rate, has increased nearly 50 basis points to 3.9%.

Investment Outlook & Portfolio Positioning

Absent the conflict in Iran, our outlook continues to remain constructive, with real GDP growth and supportive consumer spending and ongoing investment in infrastructure, energy and Artificial Intelligence all expected to enhance productivity. Broadly, the global economy is still expanding, and inflation continues to moderate despite all the negative headlines. Earnings growth grew at a 12.8% clip last year and is expected to grow 13.2% in 2026, according to data from FactSet. For now, corporate profits and the broader economy continue to show resiliency despite all the gloom. However, the Iran conflict’s duration will largely determine the impact on the global economy. With the Strait of Hormuz effectively shut, 20 million barrels of oil that transit the Strait daily are stranded. This accounts for roughly 20% of daily global oil demand. Liquified natural gas (LNG) is also heavily impacted by events in the Middle East. Qatar is responsible for 20% of global LNG supply and at the moment 100% of this is offline. Any escalation that results in energy infrastructure being damaged will have lasting effects on the energy market. Oil and gas fields are not like faucets—they cannot just be turned off and on. Once they are shut in, there are engineering and geological risks that don’t guarantee their resumption at previous production levels and could take months to restart.

Understandably, the conflict in Iran has sent oil prices higher and is stirring memories of the inflationary spike of 2022 following the start of the Ukraine/Russia war. Broadly speaking, the current facts lead us to believe that today’s environment is different than from a few years ago. Rates are significantly higher, liquidity is being pulled from the system, the labor market has cooled down, and wage growth has decelerated. For the moment, any increase in inflation in the coming months or quarters will be driven by supply constraints rather than excess consumer demand. Inflation has certainly cooled in recent years; however, it remains above the Fed’s 2% target. Central Banks tend to focus on core inflation readings, i.e., those that exclude the more volatile food and energy prices. Given this, the Fed is more likely to respond to higher oil prices by holding rates where they are instead of hiking them. For now, our current base case is that the current oil shock is far more likely to produce a temporary bump in headline inflation rather than a repeat of the broad and persistent inflation cycle experienced a few years ago.

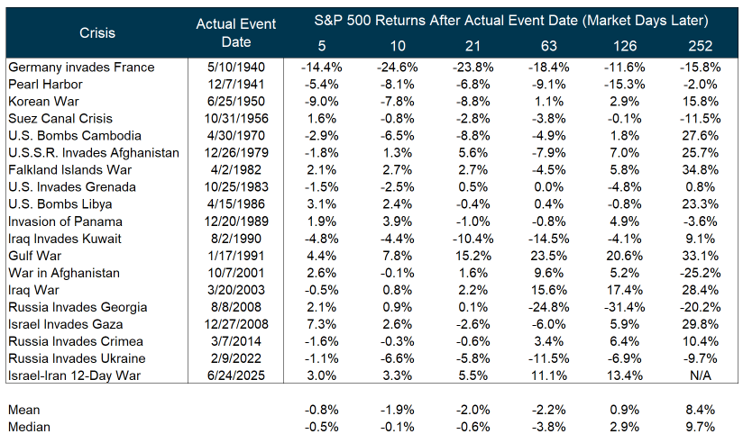

Despite all the aforementioned events, as of quarter-end U.S. stocks are only 6% off the all-time high it reached in January. While geopolitical shocks can trigger sharp drawdowns, history suggests the impact is typically short-lived. Markets tend to reprice uncertainty quickly, with most of the reaction happening over days and weeks rather than quarters or years. Unless the event materially changes the path of the economy or policy, risk assets can remain supported. The table below shows the market reaction to military events since World War II. The current conflict has certainly resulted in negative equity returns, but nothing outside the historical norm.

Source: Ned Davis Research

Despite recent weakness, equity market fundamentals remain solid. We have begun to see market leadership broaden away from mega-capitalization technology stocks to smaller and more value orientated companies, providing crucial breadth for the market. Equity valuations remain somewhat elevated and above their long-term average. Elevated valuations do not imply an imminent market downturn, but they do tend to constrain longer-term returns. Historically, periods with similar starting valuations have been followed by lower subsequent real returns over the next decade, though the historical sample is limited. Looking ahead, expect returns will be driven more by earnings durability and cash-flow generation than by further multiple expansion – reinforcing the importance of selectivity, diversification, and a focus on companies with durable earnings power and strong balance sheets. However, valuations for international stocks remain attractive and are currently trading at a meaningful discount compared to U.S. stocks. Even after a strong 2025, we see value in select international exposures given attractive valuations and the non-dollar currency exposure they provide – particularly if the U.S. dollar continues to weaken alongside Fed policy shifts and our continued high and growing level of government debt.

Credit fundamentals continue to remain sound and attractive starting yields have resulted in fixed income returns increasingly driven by income rather than price appreciation. We expect rates to stay somewhat elevated due to sticky inflation and the never-ending growth in budget deficits that lead to an increasing supply of government borrowing and bond supply. The positive side of this is that we continue to see attractive yield opportunities (5%-6%) in the fixed-income market, allowing us to capture attractive income without overreaching for return in our balanced portfolios.

Alternative or non-traditional investments continue to offer risk-reduction benefits, while providing solid return potential. Managed futures historically have performed well in high volatility environments such as this. Commercial real estate appears to be bottoming and providing some interesting upside in selective sectors (i.e. – distribution/logistics, industrial, specialty sciences, etc.), given lower supply and higher demand. Diversification and low-correlation characteristics are additional benefits, as well.

Closing Thoughts

The conflict in Iran has introduced a number of unknown variables into the investment outlook. Thus far, markets have largely looked through the clash (rebounding and approaching record highs as we print this); however, with each passing day the impact on the global economy becomes greater. There is no question the tail risks have increased as a result of the Iranian conflict, however with the range of outcomes so wide we do not believe it is prudent to make any large-scale changes as a one size solution does not fit all clients. We remain vigilant to the changing situation and thank you for your continued trust and partnership. Please also find enclosed the economic newsletter from Dr. Ray Perryman.

The Water Valley Investment Team